Ever looked at your bank statements and seen an unfamiliar transaction for NWEDI Charge on Bank Statement? When you receive an unexpected charge on your bill, it can be confusing, particularly if you don’t recognize the source of the charge. Many consumers search for answers after spotting this description because financial transaction codes often appear differently from the actual company or service name associated with a payment.

It’s essential to be familiar with what the NWEDI transaction is to handle your finances and determine if a charge is valid. Some bank statement descriptions are obvious; others employ the processing network identifiers that leave account holders confused. In many instances, the charge is related to an approved payment or subscription, or an electronic transaction that has been transacted over a payment network.

The purpose of this guide is to explain what NWEDI is, why you may see a charge like this on your statement, how to be sure you know where the charge came from, and what to do if you think the charge is unauthorized.

Understanding NWEDI Charge on Bank Statement

In general, NWEDI is the payment processing description on a bank statement pertaining to an electronic transaction routed through a particular payment processing system. Some transactions have a processor code or shortened descriptor rather than the merchant’s name.

This can cause consumers to be worried about seeing an unfamiliar charge. In most cases, the transaction is associated with an authorized, valid purchase, subscription, membership, or payment for a service that has been previously requested.

Payment processors are the middlemen between business, bank, and customer. In some cases, the processor’s identifier may be found in place of the brand name of the merchant when a transaction is completed.

Therefore, a thorough investigation of the charge is essential before accepting it as a fraud.

What Does an NWEDI Charge on Bank Statement Mean?

An NWEDI charge on bank statements is generally considered to be a charge that is made over a payment network that has other organizations accessing it or a transaction service that is undergoing an electronic payment process. The origin of the charge can change based on the merchant and the payment technique employed.

There are a few common cases that can result in such a transaction descriptor appearing:

• Monthly subscriptions

• Online purchases

• Membership renewals

• Utility payments

• Automated billing services

• Digital services

• Recurring payment agreements

Unfortunately, the descriptor does not always point to the business that received the payment. Rather, the name of the processor will be visible, and the cost will seem unrecognizable.

This can often cause the account holder to think that this is a fraudulent transaction in his account when it was actually linked to a service he uses on a regular basis.

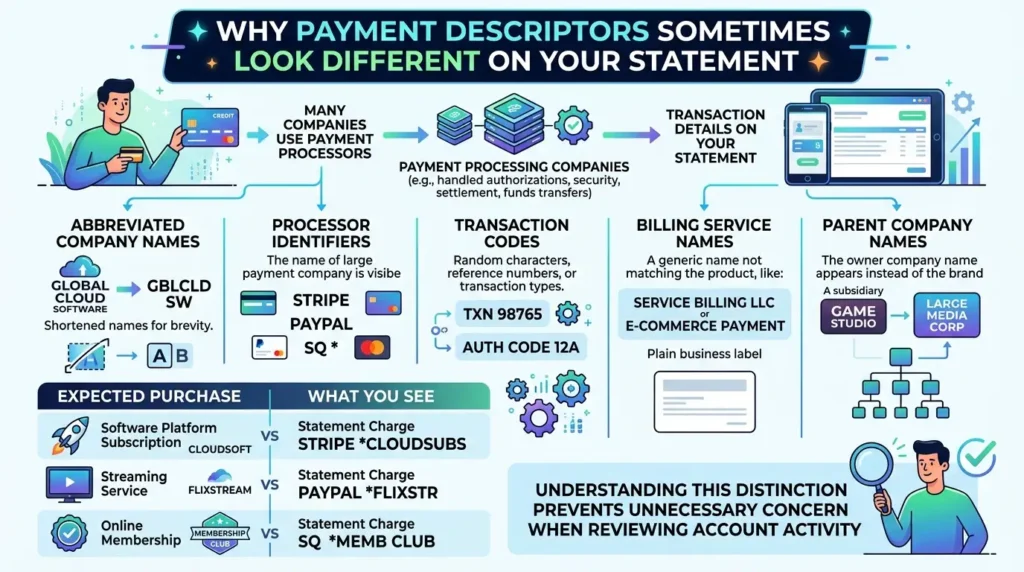

Why Payment Descriptors Sometimes Look Different

Many companies use payment processing companies. These processors deal with transaction authorizations, security, settlement, and funds transfers.

Each time a transaction is made, the details you see on your statement are dependent upon how the transaction is processed:

• Abbreviated company names

• Processor identifiers

• Transaction codes

• Billing service names

• Parent company names

This can make it hard to recognize the purchase the first time around.

For example, you may subscribe to a software platform, streaming service, or online membership, but the charge may appear under the payment processor rather than the actual service provider.

Understanding this distinction can prevent unnecessary concern when reviewing account activity.

How to Identify the Source of an NWEDI Charge on Bank Statement

If you see an NWEDI transaction and you do not know where it is from, there are a few steps you can take to determine the source of the transaction.

Review Recent Purchases

Step one is to look over your recent spending transactions. Consider:

• Online orders

• Subscription renewals

• Mobile app purchases

• Membership fees

• Automatic bill payments

Check transaction dates with purchase history, as well as the quantity of transactions and amounts.

Check Email Receipts

When payments are made, many online services will send confirmation emails. A good way to determine the merchant is to look in your mailbox for receipts in the vicinity of the transaction.

Look for:

• Order confirmations

• Subscription renewal notices

• Payment receipts

• Membership billing emails

Review Recurring Payments

Recurring subscriptions that consumers signed up for months or years ago are ones that they often forget about.

These are just a few of the usual repeating fees that you may encounter:

• Streaming platforms

• Cloud storage services

• Fitness memberships

• Software subscriptions

• Digital content providers

Check your ongoing subscriptions to see if the purchase is of one of the following services.

Contact Your Bank About an NWEDI Charge on Bank Statement

If you still cannot determine the charge, get in touch with the bank directly. Financial institutions may be able to give more information about the transactions, such as:

• Merchant information

• Transaction location

• Processing details

• Authorization records

This extra detail can all too easily solve the puzzle.

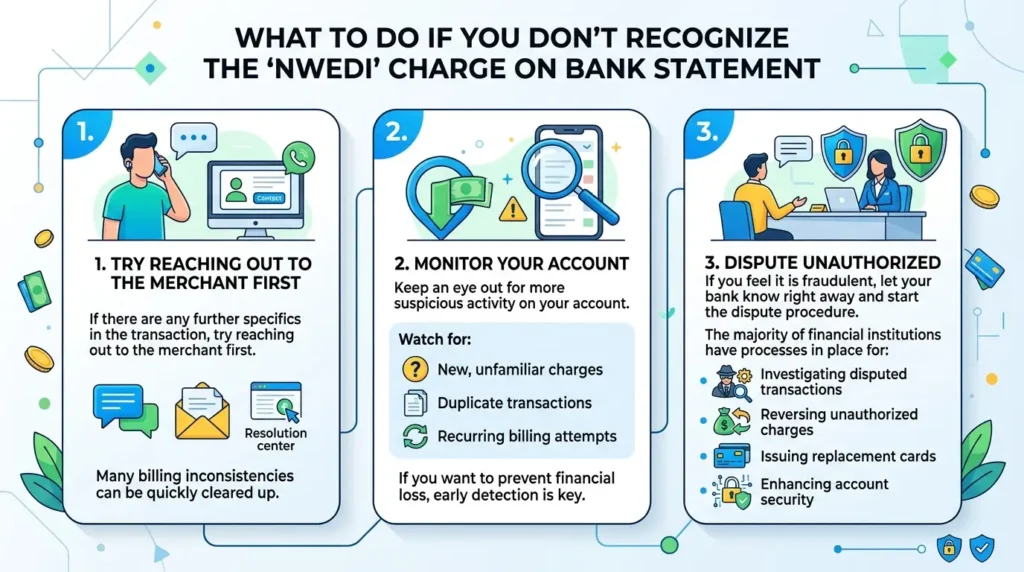

What to Do If You Don’t Recognize the NWEDI charge on bank statement

If there are any further specifics in the transaction, try reaching out to the merchant first. There are a number of billing inconsistencies that can be quickly cleared up.

Monitor Your Account

Keep an eye out for more suspicious activity on your account.

Watch for:

• New, unfamiliar charges

• Duplicate transactions

• Recurring billing attempts

If you want to prevent financial loss, early detection is key.

Dispute Unauthorized Transactions

If you feel it is fraudulent, let your bank know right away and start the dispute procedure.

The majority of financial institutions have processes in place for:

• Investigating disputed transactions

• Reversing unauthorized charges

• Issuing replacement cards

• Enhancing account security

Conclusion

Seeing an unfamiliar NWEDI transaction on your statement can certainly raise questions, but in many cases, it simply represents a legitimate payment processed through a third-party billing network. The transaction description may not be immediately recognizable due to the fact that payment processors are sometimes substituted for merchant names. When you see the NWEDI Charge on bank statement, go through your purchases in recent months, monitoring for any unauthorized charges, and search for emails of subscription renewals and payment confirmation.

FAQs

1. What is an NWEDI charge on a bank statement?

An NWEDI charge on a bank statement is usually an electronic payment processed through a third-party payment network. The charge may appear under the processor’s name instead of the actual merchant.

2. Is an NWEDI charge a sign of fraud?

Not necessarily. In many cases, the charge is linked to a legitimate purchase, subscription, membership renewal, or online payment. However, if you do not recognize it, you should investigate further.

3. How can I find out which company made the NWEDI charge?

You can review recent purchases, check email receipts, look at recurring subscriptions, and contact your bank for additional merchant details associated with the transaction.

4. Why does the NWEDI charge not show the merchant’s name?

Some businesses use third-party payment processors. As a result, your bank statement may display the processor’s identifier, such as NWEDI, rather than the company’s name.

5. What should I do if I believe an NWEDI charge is unauthorized?

Contact your bank immediately, monitor your account for additional suspicious activity, and file a dispute if you believe the transaction was made without your authorization.