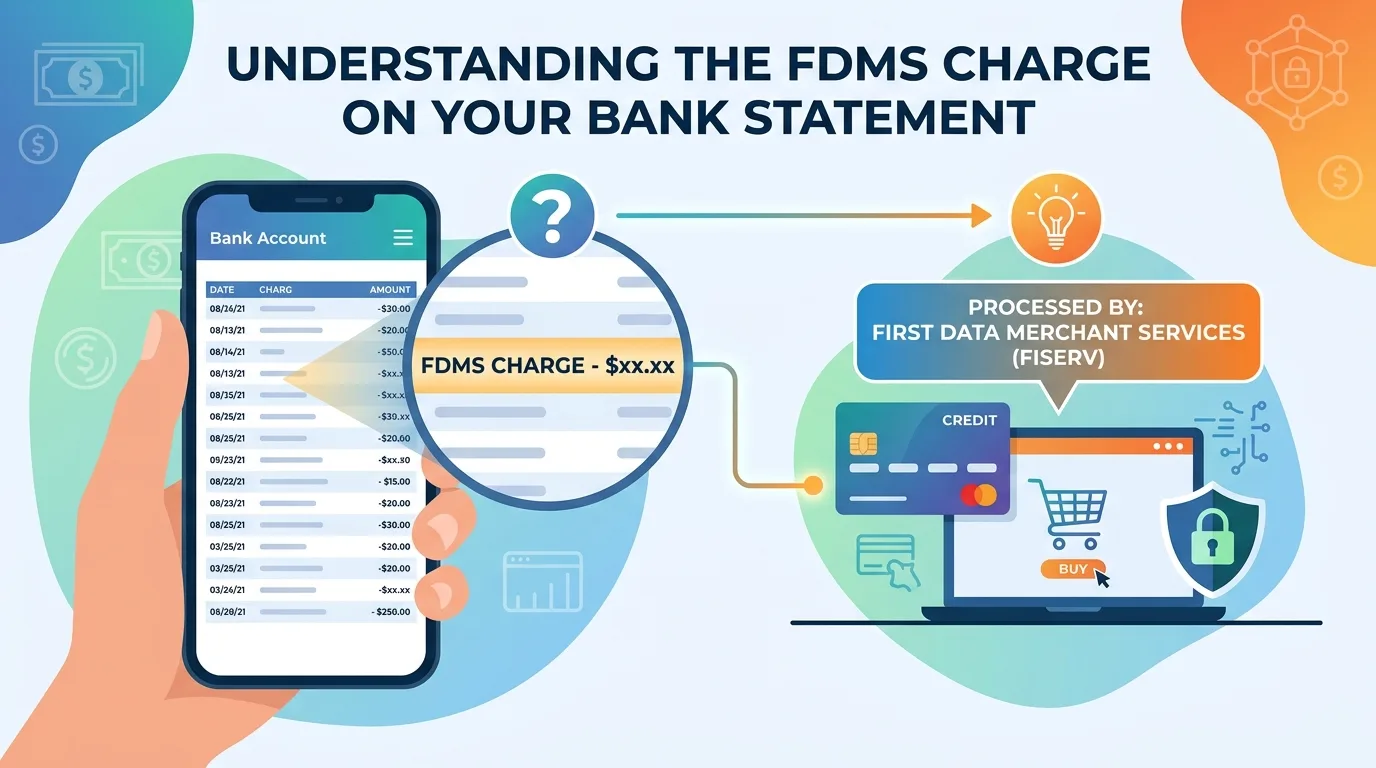

If you’ve checked your bank account recently and found an FDMS charge that you don’t recognize, you may be wondering if it’s something you need to worry about. Even if you shop online frequently, unfamiliar charges on your bank statement can still be concerning, with all the ways we make digital payments or use them in everyday life.

Generally speaking, an FDMS charge is a valid charge from a merchant who has processed your payment through First Data Merchant Services, now called Fiserv. Fiserv offers merchants throughout the United States a way to accept debit cards, credit cards, and digital payments.

If you learn more about FDMS charges, you will be able to identify whether or not you made a legitimate purchase from a merchant, determine if there was an error with billing, and avoid potential fraud. In addition, the following article will explain what FDMS is and why you see an FDMS charge on bank statements, and what you should do if you do not understand an FDMS charge.

What Does FDMS Mean?

First Data Merchant Services (FDMS) is a widely used credit/debit card processing system (formerly known as First Data) that is now part of Fiserv’s payment processing platform. Fiserv processes electronic payments for thousands of U.S. businesses.

When you use a credit card, debit card, mobile wallet, or another form of payment online, many people are working behind the scenes to process your payment. One of these entities is FDMS, which processes the payment on behalf of your financial institution and facilitates the transfer of funds from your financial institution to the merchant.

As a result of this processing, there will be some transactions on your statement with “FDMS” instead of the name of the store where you shopped. This can be confusing for many consumers when they see an “FDMS” purchase on their statements, because they may not have made the purchase themselves.

In most cases, an “FDMS” charge on your bank statement is an indicator that you purchased with a merchant who processed their payment through Fiserv.

Why Does an FDMS Charge Appear on Your Bank Statement?

There can be several reasons why these FDMS charges may appear confusing to you:

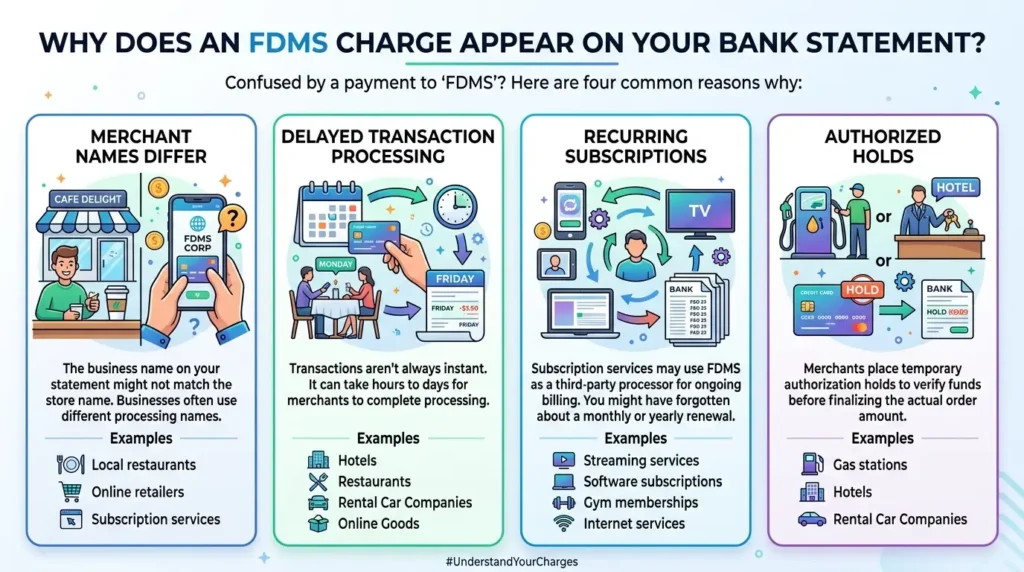

· Merchants May Have Different Names

The business name on your statement might not be the same one that you recognize from a store. Many businesses use a different name for processing payments. For example, a local restaurant, online retailer, or subscription service might use a different name than the actual business name when they process your payment.

Because of this, it may be difficult to find legitimacy in an FDMS purchase at first glance.

· Delayed Processing of Transactions

You also need to keep in mind that many businesses do not complete the processing of your transaction immediately. Hotels, restaurants, rental car companies, and some merchants that sell goods and services online may take anywhere from a few hours to several days before they process your payment in full.

Consequently, an FDMS charge on your bank statement could show up days after you made the actual purchase; therefore, it will be hard for you to relate that particular charge to the recent purchases.

· Recurring Subscription Charges

Some subscription services utilize third-party payment processing companies for ongoing payment processing. This can include streaming services, software subscriptions, gym memberships, and many other forms of internet services, and subscription charges may be for the continued payment processing of FDMS.

If you’ve forgotten about a monthly or yearly subscription renewal, then the FDMS charge may not be something you are expecting.

· Authorized Holds

Some merchants will place a temporary authorization hold on an order before they finalize the actual amount of the order. You will typically see this at gas stations, hotels, and rental car companies.

In some cases, FDMS transactions are related to other payment processing entries such as the NWEDI charge on bank statement, which may appear due to similar financial networks.

Is an FDMS Charge on Bank Statement Legitimate?

Under normal circumstances, yes; an FDMS charge indicated on your bank statement is typically related to a legitimate purchase made through a merchant that processes its payments with Fiserv.

It is also typically common to find an FDMS charge on bank statements, as Fiserv processes billions of payments for merchants all over the country.

However, you should not just assume that any FDMS charge is automatically valid; always verify verification of any unfamiliar payment on your bank statement by reviewing your recent purchase history, receipts, and subscriptions.

How to Identify an Unknown FDMS Charge on Bank Statement

If you don’t identify an FDMS charge on your bank statement, there are several things you can do to find out what it may be.

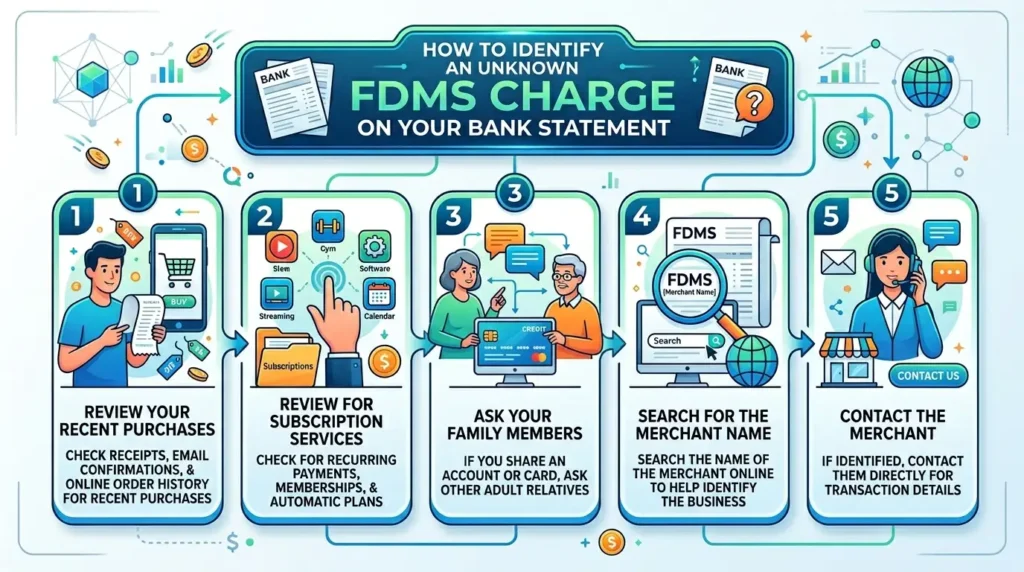

· Review Your Recent Purchases

Check your receipts, email confirmations, and online order history for purchases made around the same date and value as this transaction.

· Review for Subscription Services

Recurring subscriptions, memberships, and Automatic Payment Plans can also be confusing if they are forgotten. Check for any that you may have forgotten about.

· Ask Your Family Members

If you and an adult relative share an account or a card, it is possible that they made this purchase without you knowing it.

· Search for the Merchant Name

Sometimes additional merchant information is provided on the statement. Quickly search the name of the merchant to help identify the business associated with this transaction.

· Contact the Merchant

If you can identify the merchant, contact them directly to get more information regarding this transaction.

You may also come across similar unfamiliar entries like the GPC EFT meaning on bank statement, which is often linked to electronic fund transfer processing.

What Should You Do If You Suspect Fraud?

Although most FDMS transactions are legitimate, fraudulent transactions can occur with every payment system. If you believe that the transaction is fraudulent:

· Contact Your Bank Immediately

If you are the victim of fraud, contact your bank or credit card issuer right away. Most banks have fraud departments and are always available to assist you.

· Monitor Your Account

After contacting your bank, check the rest of your recent account activity to find any other potential fraud.

· Block or Replace Your Card

If your bank has determined that the card may have been compromised, they will typically close out the current card, do not use that card again for any transactions, and give you a new account to use for future transactions.

· File a Dispute for Unauthorized Transactions

Consumers may dispute unauthorized transactions on their bank accounts when a financial institution offers consumer protections. The sooner a consumer disputes fraudulently transacted funds, the timely and more efficient, the institution’s investigation will be.

How to Prevent Future Confusion About FDMS Charge on Bank Statement

Consider adopting a few habits to prevent uncertainty over future FDMS charges on bank account entries:

· Digital receipts should be maintained for all online purchases.

· A budgeting application should be utilized to track recurring subscriptions.

· A financial institution should have transaction alert notifications enabled through its banking application.

· Regular reviews of an individual’s bank account should be conducted.

· Large expenditures and travel-related expense records should be maintained.

By conducting these activities, all of which are common practices, identifying valid transactions and suspicious activity should be relatively simple.

Conclusion

Finding an unfamiliar FDMS charge on a bank statement can sometimes be perplexing, but it can often be linked to a valid transaction processed by Fiserv. As FDMS serves as a payment processor for a multitude of merchants across the country, the transaction could simply represent a purchase from a retailer, restaurant, online retailer, or subscription service.

Before assuming fraud has taken place, a consumer should first check the recent purchases and/or subscriptions and receipts to determine if the transaction(s) can be traced back to a valid transaction. If customers are unable to identify the payment or believe the transaction occurred fraudulently, they should promptly contact their bank to protect their account and to initiate an investigation.

By having a sound understanding of how the FDMS payment processing system works, consumers will feel more comfortable interpreting their monthly bank statements and become better able to manage their own personal finances.

FAQs

1. What is an FDMS charge on my bank statement?

An FDMS charge is usually a payment processed through First Data Merchant Services (now Fiserv). It means you made a purchase from a business that uses Fiserv to handle card payments.

2. Why does an FDMS charge appear instead of the merchant’s name?

Many businesses use different payment processing names than their store names. Because of this, your bank statement may show “FDMS” rather than the business where you made the purchase.

3. Is an FDMS charge always legitimate?

Most FDMS charges are legitimate and linked to real purchases. However, if you do not recognize the transaction, review your receipts, subscriptions, and recent purchases before contacting your bank.

4. How can I find out which merchant made the FDMS charge?

Check the transaction date and amount, review your email receipts, look through subscription payments, and search for any merchant details listed on your statement. You can also contact your bank for more information.

5. What should I do if I think an FDMS charge is fraudulent?

Contact your bank or card issuer immediately, report the suspicious transaction, monitor your account for other unauthorized charges, and request a replacement card if necessary.