When you receive your bank statement and discover unknown transactions, it is easy to feel overwhelmed or shocked. Consumers frequently see unfamiliar transactions like this one (ABSydney, Acquisitions Bank of America). The most common example of this type of transaction abbreviation is the ‘SP AFF’ charge. If you see an SP AFF charge on a bank statement, don’t panic. You may be seeing this new billing name as well because it is simply a shorthand version of the abbreviated consent.

Today’s digital world is filled with subscriptions, e-payments, automatic bill payments, etc. Many of these fee names/abbreviations are vague or just misleading, so there is no way for consumers to know if the fee name on their statement represents an actual company or simply a method of payment. In addition, each of the companies will use different methods of reporting these transactions to the bank or payment processor, so many do not have the same company name on the statement to reference when trying to determine which company the transaction is for (i.e., a bank may not use the same name as the parent company).

This article will explain to you what these charges are, why they are being charged, whether or not they are safe or suspicious, and what steps to take if you don’t recognize them. The information can help to prevent unnecessary anxiety and better control finances.

Understanding SP AFF Charge on Bank Statement

SP AFF is generally an abbreviation of a payment processor or third-party billing system transaction label. It does not typically come from your financial institution or as a regular fee. Rather, it’s a virtual transaction tied to an outside merchant or service.

When a transaction passes through affiliate billing networks, the SP AFF will show on the bank statement. These systems are used to accept payments for different online services, apps, and subscriptions. The bank statement is likely to contain only a truncated payment processor name, as a number of merchants can share the same account.

Many of the users find it difficult to immediately recognize the source. It doesn’t indicate which company charged you the bill, but instead it verifies that a digital payment was made.

Most identifications of SP AFF resemble the submission of reputable services (streaming service, subscription software, etc.) using a third-party payment method. SP AFF charges are often related to digital billing systems and may appear alongside entries such as the PNP Bill Payment charge on bank statement, which is commonly seen in automated payment processing.

Common Reasons You See SP AFF Charges on Bank Statement

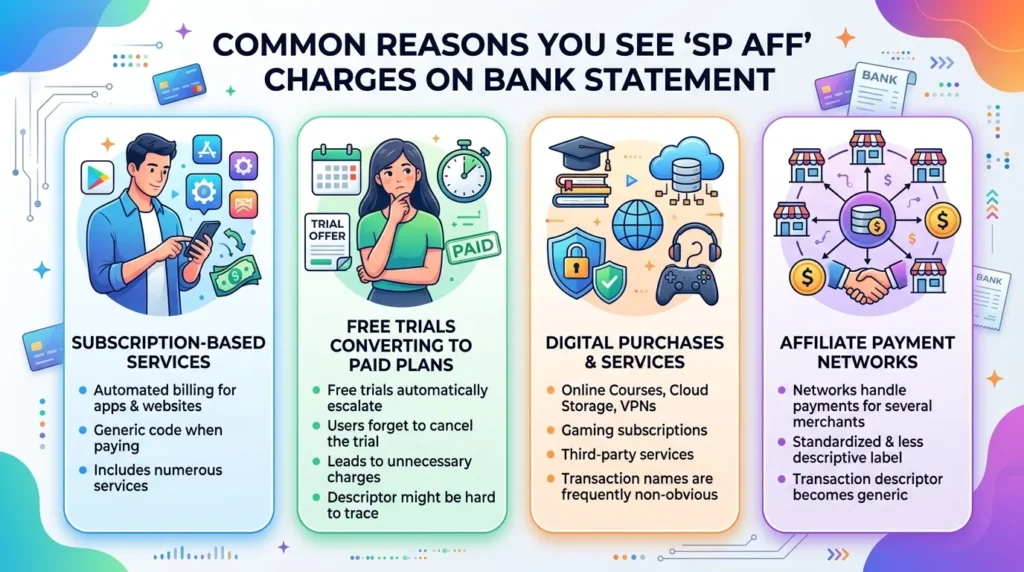

There are several different reasons an SP AFF could appear on your bank statement. This is one of the most common reasons, namely, the subscription-based services. Numerous apps and websites allow for automated billing and may show up with a generic code when you pay.

Another is free trials, which automatically escalate to paid plans. The users forget to cancel the trial, so they get unnecessary charges. If this occurs, the billing descriptor might appear on the bank statement as an SP AFF charge and be more difficult to trace off the bat.

It can also apply to digital purchases, like online courses, cloud storage, VPN services, or gaming subscriptions. Services are frequently third-party, and transaction names aren’t apparent.

In some instances, there are networks of affiliate sites that take care of payments for several merchants. In this case, the transaction label turns into a standardized and less descriptive label.

Find Out If SP AFF Is A Safe or Suspicious Charge on Bank Statement

In the majority of situations, SP is a valid transaction tag that payment systems use. It doesn’t necessarily mean you’ve been cheated or had your account accessed without permission. Despite the name being unclear, it can sometimes be seen as suspicious to the user.

If you see recent subscriptions or online purchases, then this is probably fine. Some digital platforms to avoid processor restrictions will include only their short name and not the full name on your bank statement.

Alternatively, if you do not have a memory with regard to the purchase, then the SP AFF charge, combined with the bank statement, should be looked at. Some tell-tale indicators are deductions that are repeated, suspicious amounts, or numerous similar deductions over a short time.

Most banks will suggest that their customers check on their recent activity before acting on a suspicion that it is fraud. If the charge is not clear, it’s best to reach out to customer support.

Most of the time, it is due to a trial expiration/authorization over the course of a month. You must check through these accounts for potential candidates.

How to Identify the Source of SP AFF on Bank Statement

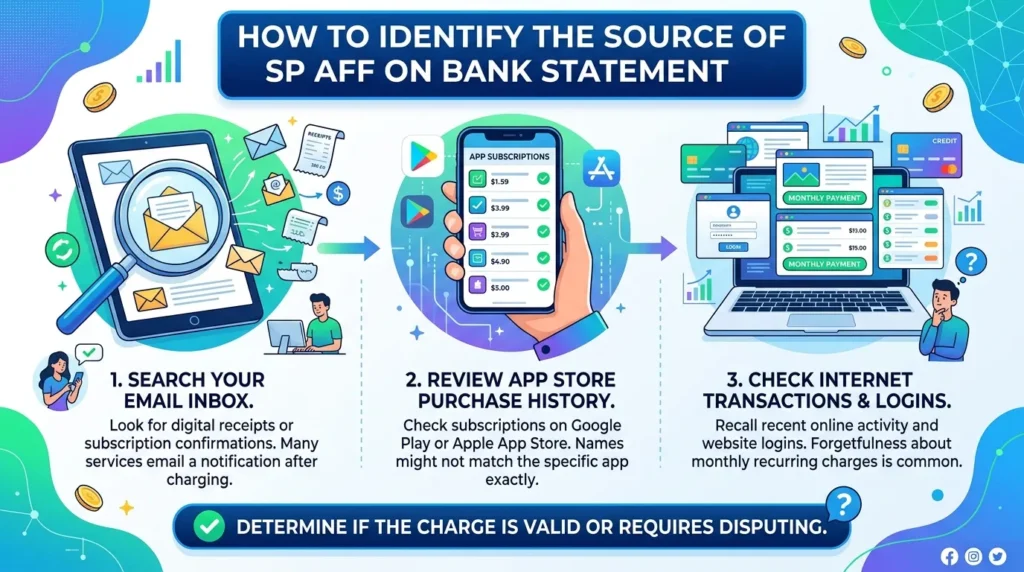

To identify where the SP AFF charge on bank statements originated from, you must review some of your recent financial and digital activity. Start by searching through your email inbox for receipts and/or subscription confirmations. Most of the time, the subscription provides an email notification once the payment is submitted.

Next, review previous transactions in your respective app stores if you utilize mobile apps for viewing your purchase history. Various app subscriptions may be associated with Google Play or Apple subscriptions, but may not necessarily have the same name as the purchased app.

You should also review one of the previous transactions via the Internet (keeping records of your previous logins). It is common for users to forget about their monthly subscriptions.

If you perform the actions above on time, you could identify whether the charge is valid or requires disputing the charge.

What to Do If You Do Not Recognize the SP AFF Charge on Your Bank Statement

The best way to determine the cause of SP AFF is to look at the financial and digital activity from the past few days. Firstly, see if you’ve received any confirmation emails or receipts in your email inbox. The major online service providers will notify you of a billing when payments are made.

Next, review app store purchases if you use mobile applications. Many subscriptions are sold via Google Play or iTunes, and the billing descriptor might not be the same as the app name.

Stroll through your browser’s saved accounts and history for providers you might have registered for. One thing that folks tend to forget about is the low-cost subscriptions; they’re paid on a monthly basis.

These steps will allow you to immediately know if the charge is valid or if it should be disputed. In some cases, users also notice similar billing entries like the OF LONDON GB charge on bank statement, which may appear due to processed or third-party payment systems.

Conclusion

The presence of SP AFF Charge on bank statement can be quite difficult to interpret sometimes; however, it generally refers to a legitimate online payment transaction that was processed by a third-party company, not as a direct fee charged by your bank, but rather as a descriptive label for those charges created by either an e-commerce site or payment gateway provider.

Due to the lack of clarity provided by these descriptions, it is essential to check on every instance and to be diligent about verifying them against subscriptions and contact your bank for help if this can’t be quickly resolved.

FAQs

1. What does SP AFF stand for on a bank statement?

SP AFF is a shortened billing label used by third-party payment processors. It does not represent a specific company name but indicates that a digital transaction was routed through an affiliate or external billing network on behalf of a merchant.

2. Can an SP AFF charge on my bank statement be from a free trial?

Yes. Many online platforms convert free trials into paid subscriptions automatically. If you signed up for a trial and forgot to cancel, the resulting charge may appear on your bank statement under a generic label like SP AFF rather than the actual service name.

3. How long does it take for an SP AFF charge to appear on my bank statement?

In most cases, the charge posts within 1–3 business days. However, depending on your bank and the payment processor involved, a temporary authorization hold may appear first before the final transaction amount is settled.

4. Should I cancel my card if I see an unrecognized SP AFF charge?

Not immediately. First review your recent subscriptions, app purchases, and email receipts to verify whether the charge is legitimate. Only contact your bank to cancel or freeze your card if you are completely unable to identify the source and suspect unauthorized access.

5. Will disputing an SP AFF charge affect my account or credit score?

Filing a dispute with your bank for an unrecognized charge does not directly impact your credit score. Your bank will investigate the transaction and may issue a temporary refund while the review is in progress. If the charge is found to be valid, the amount may be reapplied to your account.